If you were born after the late 1990s… you must have heard this word:

👉 SIP (Systematic Investment Plan)

And yes… it is the favorite word of YouTube finfluencers.

Why?

Because it is simple to say… simple to show… and feels like a shortcut to becoming rich.

You must have seen something like this:

- 👉 Invest ₹5,000 every month

- 👉 Get 12–13% return

- 👉 Become a crorepati… maybe even more

Calculator bhi same bolta hai.

So the question is…

👉 Does SIP really make you a billionaire?

If we trust the calculator blindly… the answer is yes.

But real life doesn’t work on a calculator.

Real life comes with small, hidden things… which are never shown in those examples.

The Reality Check: Calculator vs. Real Life

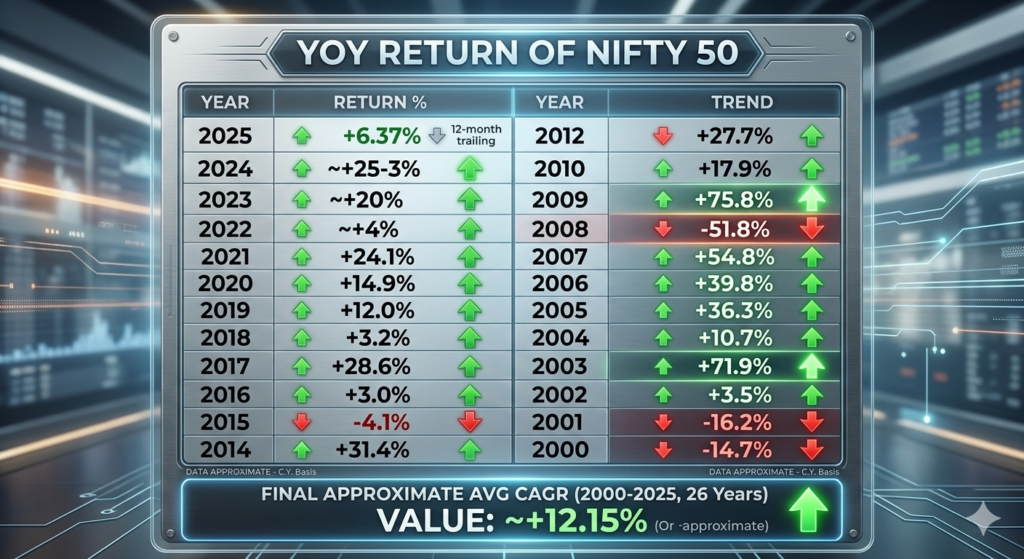

1. Returns are never clean

When someone says “12–13% return”… it looks like a fixed number.

But the market doesn’t work like that.

- Some years the market gives very high returns.

- Some years it gives nothing.

- And some years it goes negative.

Even the long-term performance of NIFTY 50 is not a straight 12.5% line. It is full of ups and downs.

But when we calculate… we assume smooth growth.

That’s the first gap between expectation and reality.

2. The cost of investing is always there

Every mutual fund charges an expense ratio.

Maybe 0.5%… maybe 0.75%…

Looks small.

But when you stretch this over 20–25 years… this small number quietly reduces your return.

And when the return reduces even slightly… the time required automatically increases.

3. Taxes will come at the end

Let’s say after 25 years… you invested around ₹15 lakh, and your value becomes ₹80–90 lakh.

Looks great.

But when you redeem… tax will apply on the gains.

So whatever number you saw in the calculator… that’s not what you actually take home.

The Most Ignored Part: Inflation

India sees roughly 6% inflation every year.

Which means… money is losing value every year.

If after 25 years you reach ₹1 Crore…

The actual purchasing power of that ₹1 Crore will feel like ₹25–30 Lakh in today’s terms.

This is where most dreams break.

Because the number looks big… but the purchasing power is not.

The Real Challenge: Human Behavior

Until now… we only talked about numbers.

But the real challenge is not numbers. The real challenge is behavior.

Because staying invested for 25 years is not easy. Life will happen in between:

- Job changes

- Unexpected expenses

- Emergencies

And data shows most people don’t continue their SIP for long.

Then comes a market crash. It will happen. It has happened before:

- 2008 crash

- COVID crash

The market can fall 40–50%.

At that moment… your long-term portfolio turns red.

And that’s where most people exit.

Not because SIP is wrong… but because staying invested becomes emotionally difficult.

Is SIP alone enough to make you a billionaire?

So now if we connect everything:

- Returns are not fixed

- Costs reduce returns

- Taxes reduce final value

- Inflation reduces purchasing power

- Behavior breaks consistency

Then the question becomes clear:

👉 Is SIP alone enough to make you a billionaire?

Answer is…

👉 No.

SIP is not a magic formula. It is just a tool.

It works only when:

- Your income grows

- Your investment amount increases

- You stay invested in bad times

Conclusion

SIP looks simple on a screen… because numbers look smooth in a calculator.

But real life is not smooth. It has noise… fear… breaks… and uncertainty.

At the end…

- 👉 SIP doesn’t fail

- 👉 People fail to stay with SIP

“It’s not about starting an SIP…

it’s about staying when it stops feeling good.”

No comments yet.

Be the first to share your thoughts.